The National Association of REALTORS® released its 2026 Home Buyers and Sellers Generational Trends Report this week. Inman's headline was "Baby boomers dominate the market as first-time buyers hit record low." That is a true statement. I have chosen a different headline, because I have been sounding the alarm on lack of affordability and its impact on our industry, on our country, and our society for years now.

Back in 2011, I wrote this post about #GenerationScrewed. There are links in there to other pieces I wrote about that generation.

You can search this site for other pieces I've written getting increasingly concerned about how younger generations and working people are getting more and more shut out of the American Dream. But here are two that may be most directly relevant:

In the Kids Are NOT Alright post, I warned about the rage and despair of younger generations. I posted this video from two years ago. It remains timely today:

And in case you think this is about socialism infecting young minds, or Mamdani supporters who just want a Communist utopia, here's someone who cannot be described as either speaking on this exact topic:

Now comes news that first-time homebuyers only make up 21% of home purchases, the lowest ever recorded by NAR since it began this series, while Boomers jumped up to 42% of all buyers, tied with last year for the highest ever recorded.

How are we supposed to feel about that news?

I guess it depends on your assumptions. If you assume that economic hardship are just part of life, and that young people will just buckle down, work harder, deal with it, and eventually somehow things will get better... then there is no real reason for concern.

If, on the other hand, you assume as I do that unsustainable systems cannot continue one way or another... then you have every reason for concern. Turns out, there is an actual economic principle called Stein's Law: If something cannot go on forever, it will stop. The only choice we have is the form in which that will stop.

At the risk of being redundant... because frankly it is, let me sound the alarm once again. This issue is important enough to repeat myself over and over. Let me point out that the conventional wisdom on this, as articulated by NAR, is... well... let's call it "incomplete."

This is a public post since the topic is of such wide public interest.

The NAR Report and the Spin

I've gone through the whole report. There isn't anything shocking in it; merely a confirmation of past trends continuing. Let me embed it for you for convenience in case you want to pore through it yourself.

The headline is right there on the summary intro to Chapter 1:

First-time home buyers decreased to 21% of all home buyers, a decrease from 24% last year. This year marks the lowest share since NAR began collecting the data in 1981.

To explain this, Inman quotes NAR Deputy Chief Economist Jessica Lautz:

“Historically, before the Great Recession, 40 percent of homebuyers were first-time homebuyers, while today the share is nearly half,” NAR Deputy Chief Economist Jessica Lautz told Inman. “The housing market is missing starter homes for entry-level buyers, and more smaller, affordable homes are needed to bring first-time homebuyers back in.”

Except that... the numbers in NAR's own report undermine the idea that what the housing market is missing are starter homes for entry-level buyers. Let me explain.

Starter-Home Shortage?

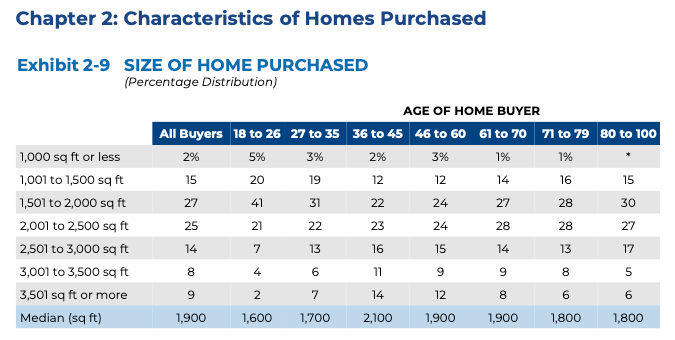

The 2026 report shows that the biggest homes in the sample — a median of 2,100 square feet — were bought not by downsizers or retirees, but by older millennials (ages 36–45), who happen to be the highest-earning generation in the country right now at a median household income of $132,700.

The typical home recently purchased was 1,900 square feet, had three bedrooms and two bathrooms, and was built in 1994. The size of homes was largest among Older Millennials, at 2,100 square feet, compared to Younger Millennials, at a median of 1,600 square feet.

The richest cohort in America is buying the biggest houses, which makes sense. Plus, the Older Millennials (in their 40s now) are the ones who likely have kids at home and need the space.

Now, the typical home purchased across the entire sample was a 3BR/2BA with 1,900 square feet built in 1994. But we get this chart:

The Boomer buyers who made up 42% of all buyers? 42% and 45% of the homes they purchased were under 2000 sq. ft. Exhibit 2-10 shows us that 24% of buyers from 71 to 79 years old bought homes with three or more full bathrooms. One wonders why retired empty nesters need three or more full bathrooms. Meanwhile, buyers from 27-35? Only 18% of them bought 3+ full bathrooms. Only 57% of them bought 2 bathrooms, while 64% of Boomers did.

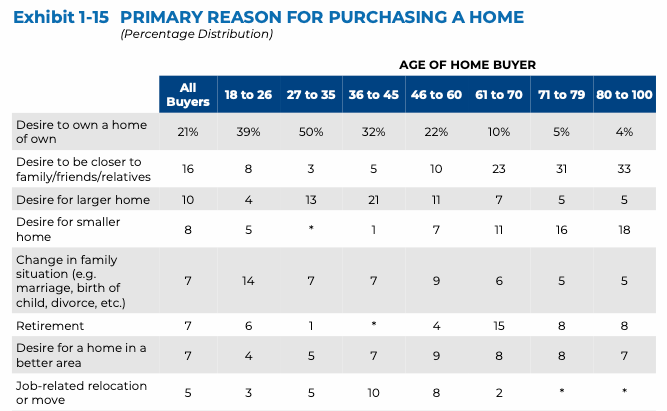

Now add on Exhibit 1-15 Primary Reason for Purchasing A Home.

I only clipped rows with at least substantial numbers in them. But for those over 60, the primary reason is to be closer to family/friends/relatives, i.e., grandkids. The second biggest reason is "Desire for smaller home" (though the 61-70 group has Retirement as the #2 reason).

There is at least a natural question that arises from these numbers. Are these retiring Boomers who want to downsize and move closer to grandkids competing against first time homebuyers for the smaller entry-level homes?

Is it ridiculous to wonder if the 28% of 71-79 year old buyers who purchased 1500-2000 sq. ft. homes had bought smaller 1000-1500 sq. ft. condos instead that more of the 27-45 year old buyers could have bought the entry-level homes?

Is it really about lacking smaller entry-level homes? Or is it about who has money to buy those homes?

Who Could Buy Entry-Level Homes?

Let's walk through some rough math, because it changes how we might think about the problem.

Take a Boomer couple who bought their move-up family home in 2011 for $300,000 — above the actual median purchase price of $220,000 that NAR reported for repeat buyers that year. I'm going with that because today's 61yo was 46 in 2011; prime earning years. This was their move-up family home in a good school district. They put 20 percent down, financed the rest around 4.5 percent (typical early-2010s rates), and refinanced in 2020 at 3 percent when their balance was about $190,000. Today, fifteen years in, their balance is about $164,000 and their monthly P&I is about $800.

Now look at what their house is worth. Case-Shiller says US home prices more than doubled from 2011 to 2026 (2.34x is the multiplier). Their $300,000 house is worth about $700,000. They sell, pay 5% in selling costs, retire the $164,000 balance, and walk away from the closing table with roughly $500,000 in cash.

Now they buy the smaller home. NAR says the median home price in America is $408,800 as of March. Entry level homes then might be $275-$300,000. Let's say this couple buys a $300,000 ranch in a retirement-friendly metro closer to grandkids. They put 30% down, slightly above the NAR median of 26% for 61–70 buyers, or $90,000. They finance the remaining $210,000 at 6.5% for 30 years. New monthly P&I: about $1,300.

So yes, the monthly mortgage on the smaller house is $500 higher than on the larger house they left.

Except that after the closing, the Boomer still has $410,000 in cash ($500K from the sale minus $90K down payment). Park it in a money market at 4.5 percent and it generates $1,538 per month in interest income. They net $238 a month to live in the smaller house, before you even count the lower utility bills, lower property tax, and lower maintenance costs.

Or... simpler still, because it would be stupid to pay 6.5% on a mortgage while getting only 4.5% from the cash, they just pay cash for the $300,000 house, as NAR's stats suggest that 39% of them do. Now they have no house-related cost, except property taxes, utility and maintenance, and still have $200,000 in cash left over.

Given the above, the house that the Boomer is buying is likely the same entry-level house that a first-time homebuyer can afford to buy.

The downsizing boomer is not bidding against the move-up buyer. They're not taking their $500K in cash and putting all of it down on a much bigger house. They're downsizing. They are bidding against the first-time buyer, except they're doing so at a major advantage. The first-time buyer, putting 3.5% down with FHA financing does not win that head-to-head.

The Real Estate Investor

That is just within the NAR study itself. Add on the question of real estate investors. There's been a lot of political hub-bub about Wall Street hedge funds and such, except they are such a tiny percentage of investor purchases across the country that they might as well not exist.

Here are the actual numbers:

- Investor share of all US home purchases has been stable at 17 to 18% for the last two years (Redfin, Q3 2025).

- Institutional single-family rental operators — the 1,000+ home class, your Invitation Homes, American Homes 4 Rent, Progress Residential — have retreated to 0.3 percent of all sales, down from a peak of 2.4 percent in 2022.

- Four of the largest SFR operators were net sellers in 2025.

At the aggregate level, the "Blackstone is buying America" narrative is empirically wrong. Institutional capital is leaving the housing market, not entering it. The actual real estate investors according to CoreLogic's 2024 tracking are overwhelmingly small landlords owning three to ten properties.

Furthermore, the blended 17 to 18 percent investor share is a national average that hides what really matters. When you look inside the low-price tier which is where first-time buyers actually shop, the picture changes.

Here's Redfin in Q1/2025:

Still, low-priced homes made up nearly half (46%) of investor purchases in the first quarter, while high-priced homes made up 30% and mid-priced homes made up 24%.

Investors also have a higher market share of low-priced homes than higher-priced homes. Investors bought 26% of all low-priced homes that sold in the first quarter, while they bought 18% of high-priced homes and 14% of mid-priced homes.

The most recent update from Q3/2025 shows stagnation, but purchase of low-priced homes was still up 1%. And any investor who runs the math ends up on the same page of Zillow, because cheap houses are the best-yielding asset.

So when we say "build more starter homes" as a fix to affordability, we should understand what we are actually proposing. We are proposing to build inventory that will be bid on by Boomers who have massive cash from the sale of their homes that more than doubled in value over 15 years, investors with 13% gross yields in their spreadsheets and cash offers in their pockets, and the young family who has a FHA loan and borrowing from Mom and Dad to put down 5% on the house. One of those three is going to win most of those bids. It is not going to be the first-time buyer.

I don't think "more entry level houses" is going to get it done.

There is no villain here. Boomers are doing what's best for them: move closer to grandkids, downsize the big family home, enjoy retirement. Investors are doing what is best for them: buy real assets with cash flows that the Fed can't print. But we do have to be honest about what this means for younger generations.

Why We Should Care

Okay, that's all fine and dandy, or doom and gloomy as the case might be, but so what? Why should we in the real estate industry care? A sale is a sale is a sale. We serve our clients, not macroeconomics.

That's true, as far as that goes. I do not believe that brokers and agents on the street should be overly solicitous of these factors. Just do what's best for your client.

Now... if you are a REALTOR, then you probably should read the Preamble to your own Code of Ethics where it talks about patriotic duty and the survival of our civilization... but that's ethics and morality, not business.

However, I have a different message for the leadership of the industry, particularly those charged with lobbying and public advocacy.

What is happening right now is nothing short of eating the seed corn. For the Boomer to have $500K in cash after selling his home, some move-up buyer has to pay $700K for that house. For the move-up buyer to be able to buy that $700K house, he has to sell his house to an entry-level buyer. If that entry level buyer is increasingly the Boomer or the investor... there is no move-up buyer to be had. Boomer selling to GenX selling to Boomer is a snake eating its own tail.

The latest numbers from NAR is that 2026 is shaping up to be below 4 million in total transactions:

Single-Family Homes in March

3.5% decrease in sales month-over-month to a seasonally adjusted annual rate of 3.63 million, down 0.3% from March 2025.

$412,400: Median home price, up 1.3% from last year.

Condominiums and Co-ops in March

5.4% decrease in sales month-over-month to a seasonally adjusted annual rate of 350,000, down 7.9% from last year.

$371,500: Median price, up 2.3% from March 2025.

I don't know if I need a degree in economics to point out that the first bullet is closely related to the second. It's a simple supply-demand-price curve. By the way, the last time we were under 4 million home sales was 1995... when US population was 266 million, not 340 million.

If young people are not buying entry-level houses, if they're not getting on the housing ladder in the first place, then it's just a matter of time before the rest of the system collapses as well.

And that's before we even talk about the impact of demographics on the type of housing demand in the future. Search this site if you want that gloomy picture.

Which means that the present moment demands a response. It demands a rethink of conventional wisdom. It demands accounting for the real economic reality confronting younger Americans, and at least a thought as to how that will shape the politics to come.

These young people may be disengaged right now. But they do vote, and more and more of them will make up bigger and bigger percentages of voters. Boomers won't live forever, despite their best efforts. At some point, it will be Millennials and Gen-Z who make up the voting population. (We Gen-X are too small to matter.)

That which cannot go on, won't. One way or another.

No Solutions, But Recommendations

Housing policy, especially affordability policy, is incredibly complicated and complex. So proposing solutions is not the point of this post. You can take a look at my idea for MADRE if you're so inclined, but I don't know if that's a solution.

But I do have recommendations for us all.

First, as an industry, we have to at least recognize that the affordability crisis is the single biggest issue we all face. It may be the biggest issue the entire country faces, but we happen to have front row seats. I believe that housing will be the spark of whatever coming revolution comes, whether via the ballot box or a different box, because it is such an obvious and simple sign of how screwed younger Americans are.

At this rate, Mamdanization of America might be the best case scenario.

Second, if we recognize that the affordability question is the most important one, perhaps we might consider finding ways to settle other questions that are far less important, far less existential, than this one?

Third, and this is specific for REALTOR Associations... I wrote this post seven years ago:

I think better late than never. If you have a YPN chapter, and that chapter is not 100% focused on this specific issue... why have one at all? Get them together in a room and charge them with the mission: figure out how to make housing more affordable for younger generations, and what YOU as YPN can do about that problem.

Let me leave it there. I suspect this problem is evergreen. We may be revisiting it in 2027.

-rsh

PS: This was from 1999. Have young people's prospects gotten better or worse since then?